Airbnb: Air Boom 'n Bust

Airbnb: Air Boom 'n Bust

Airbnb can afford the private market's expensive "late check out fee" but stewardship "costs" will persist

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

The COVID-19 pandemic forced Airbnb to raise expensive capital, but behind-the-scenes reporting point to even greater “costs” for CEO Brian Chesky as his stewardship is (anonymously) questioned by stakeholders through the media.

The cost of paying 9% to 12% interest rates on debt is trivial to the cost of regaining the trust and buy-in of stakeholders. This overhang will likely persist well after the market stabilizes and the company goes public.

Note: Airbnb’s founders famously created and sold “Obama O’s” and “Captain McCain” cereal box art as a way to fund the company during the 2008 financial crisis. That hustle and resilience won over many in Silicon Valley. Hopefully the recent fundraise with Silver Lake and Sixth Street brought on by the COVID-19 crisis brings back some of that mentality and focus.

Airbnb Forgoing the 2018 “Go Public” Window

To better frame the stewardship issues bubbling up in 2020, I think it’s important to go back to 2018 when Airbnb’s founders passed on going public.

According to the WSJ, bankers estimated Airbnb could have gone public in 2018 at a $50 billion to $70 billion valuation, but the founders opted to stay private believing the company would perform better out of the spotlight.

Bloomberg described CEO Brian Chesky’s decision to stay private in 2018 as “unapologetic”:

Chesky has been unapologetic about his ambitions to keep Airbnb private for now. “I know people will ask what these changes mean for a potential IPO. Let me address this directly. We are not going public in 2018,” Chesky said in a statement announcing Johnson’s promotion [to COO] and [CFO] Tosi’s departure on Thursday. “We will make decisions about going public on our own timetable.”

Some directors also believed Airbnb was missing important pieces (i.e. independent directors, CFO, and other key executive leadership) to go public, and the cash runway risks appeared manageable given the business was profitable and had $5.5 billion of cash.

Overall, the decision to stay private in 2018 wasn’t unreasonable, but it did ramp up “palace intrigue”.

“Founder Friendly” Control and “Palace Intrigue” Risks

Palace Intrigue: A situation in which powerful individuals within an organization are working against each other. (source)

There are advantages to staying private and operating “out of the spotlight”, but it also comes with what I call “palace intrigue” risks.

Founders are basically Emperors due to their near-absolute “founder friendly” control of the company and VCs are like the Senate advising the Emperor.

As long as the company’s core business is growing in-line or above expectations, founders are usually given a lot of freedom to pursue a wide range of strategies and growth investments.

There may be dissenting views among investors, but those concerns tend to stay in the background as long as valuations are moving in the right direction. Even if investors want changes, there’s generally not much they can do.

But if the company is running out of cash and/or the core business begins to stall or falter, it creates an opportunity for investors to proactively step-in and push for changes.

Suddenly, whatever “long term” strategic initiatives the founder was pursuing can be taken off the table and there’s a lot of pressure to “clean up” the company. In extreme cases, the knives come out and “Caesar gets stabbed in the back” (founder is removed).

“Palace intrigue” tends to intensify the longer a company stays private. Unlike in public markets where patient capital compounds, private market capital turns more impatient with the passage of time.

Late-Stage Markets: When Patient Capital Turns Impatient

I think many overestimate just how “long term” late-stage private markets can be and underestimate the public market's ability to catalyze and support “long term” mandates for those who earn it.

Late-stage private markets can feel “long term” (and liquid) as long as the company sees a step-up in valuation every 12 to 18 months, but if/when valuations begin to flatten or materially drop due to market dislocation (or company-specific issues) late-stage capital can quickly turn illiquid, expensive, and put the company on a “short term” quarterly cadence.

Most late-stage companies in this COVID-19 environment will likely be forced to accept dilutive or ratchet heavy deals that they can’t refuse (if they’re lucky to get a deal at all). Others may “kick the can” raising debt, but still face valuation high watermark issues down the road.

Luckily for Airbnb, they can afford to pay the expensive debt to avoid highly dilutive equity, but the question is would they even be paying 9% to 12% interest rates if they went public in 2018? I suspect they wouldn’t, but that’s speculation on my part.

For reference, Booking.com was able to raise debt at 4.1% to 4.625% and the stock has shown recent resilience (although down ~30% YTD) despite room night reservations down 85% from a year ago.

Chaos is a Ladder: Airbnb’s Unexpected Cash Runway Problem

In a normal environment, Airbnb does not have a cash runway issue. When the founders decided to stay private in 2018, fundraising risks was probably not top-of-mind and I surmise they believed there was more “risk” to the company’s long-term vision going public than staying private.

Unfortunately for Airbnb, the precipitous drop in revenue/demand due to COVID-19 combined with ramping operating expenses would unexpectedly expose the company to cash runway risks and force a capital raise.

While I expected Airbnb to have liquidity and fundraising challenges due to COVID-19, I did not expect to see “palace intrigue”. I was genuinely surprised to see CEO Brian Chesky (reportedly) being pressured to reduce fixed costs and upgrade management:

As the saying goes, “chaos is a ladder” and the chaos of COVID-19 created an opportunity for investors to push for change.

Bad Luck vs. Bad Stewardship

I initially thought the Airbnb saga was a “bad luck” story due to COVID-19, but reporting from the WSJ (that Airbnb is disputing) indicates there’s a “bad stewardship” story here too:

Some investors declined to put in new money after Airbnb said it wouldn’t replace Mr. Chesky as chief executive, while others didn’t participate because they didn’t think the terms were favorable, according to people familiar with the terms of the deal.

Some investors said they would put up money only if Mr. Chesky reduced his voting control and either relinquished his CEO job or work alongside a turnaround executive, the people familiar with the deal negotiations said.

I don’t know if CEO Brian Chesky is actually a bad steward or needs to be replaced, but the narrative is out there now.

It’s extraordinary to see investors this publicly critical (albeit anonymously) of Brian Chesky’s leadership.

That alone should raise some flags, but what really caught my attention was the active involvement of independent directors:

Some board members, led by independent directors Kenneth Chenault, the former American Express chief executive, and former Disney executive Ann Mather, intensified their push to get Mr. Chesky to cut costs, according to people familiar with the board.

It’s not often you see reports of independent directors being the ones leading the charge on cost cuts and rationalization, especially in VC-funded companies. Most board friction occurs between founders and investors so to see independent directors get involved is unique and raises more questions.

Overall, I can’t help but ask why are:

New investors requesting verbal commitments from the company to reduce its fixed costs and to strengthen its management.

Existing investors requesting management changes and reluctant to invest more capital due to Brian Chesky’s continued tenure as CEO.

Independent directors are pushing for cost cuts.

That is a lot to take in and and those questions will persist well past COVID-19 and when the company eventually goes public.

The Emperor Doesn’t Listen to Anyone

A possible glimpse into why investors and independent directors are frustrated with CEO Brian Chesky’s leadership may be seen in his handling of consumer refunds during the COVID-19 crisis:

Mr. Chesky approved the rollout of the new [refund] policy: Airbnb would refund any stay booked on or before March 14, with a check-in date between March 14 and April 14. Airbnb later extended the check-in date to May 31. The move was a drastic overhaul of the company’s longtime practice of allowing hosts to set their own cancellation policies and stick to them, no matter what the circumstances.

He didn’t notify board members before making the change, according to people familiar with the situation. Some were miffed they weren’t consulted and felt the decision to pay cancellation fees was hasty, these people said.

First, I think changing the refund policy was absolutely the correct decision.

The problem is CEO Brian Chesky shouldn’t be making decisions of this magnitude unilaterally without notifying the board. That is bad stewardship and a governance disaster waiting to happen, even if it ends up being the right decision.

It’s the sort of action that gets founders forcibly removed, and actually makes me wonder what else is the board not being properly informed about.

Right Sizing the Organization

I suspect CEO Brian Chesky was already feeling pressure to right size the organization before the COVID-19 pandemic.

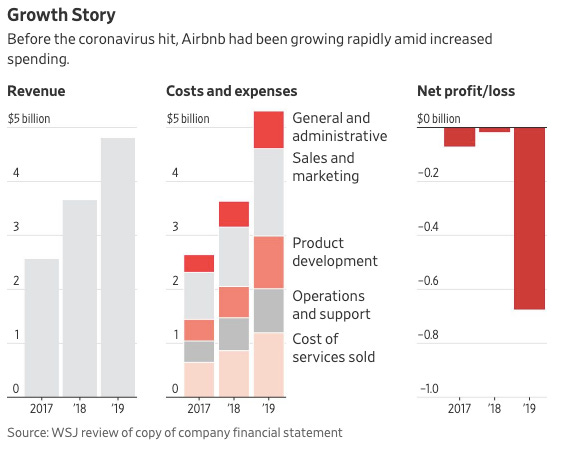

When Airbnb decided to stay private in 2018, the company had exceeded financial projections for 2017 and riding a lot of momentum. The company was forecasting (in 2017) that it would achieve $8.5 billion in revenue and $3.5 billion EBITDA by 2020.

I have no visibility into Airbnb’s financial planning process, but it’s not a stretch to presume Airbnb’s board agreed to ramp operating expenses in 2018 and 2019 based on management’s robust revenue and EBITDA expectations.

As operating expenses ramped up, without a requisite lift in revenue and profitability, I can see that causing friction between CEO Brian Chesky and the board/investors. It would actually explain a lot of the frustration and criticism being reported by the WSJ.

Is cutting fixed costs the right thing to do or are there under appreciated “long term” considerations that justify staying the course and the cost base?

It’s hard to say from the outside, but you can learn a lot about the authenticity of “long term” opportunities by the way employees react/respond.

The Emperor Has No Clothes!

When Steve Jobs returned to Apple as CEO in 1997, he described the positive reaction employees had when Apple cut 70% of the product line:

“I came out of the meeting with people that had just gotten their projects canceled and they were three feet off the ground with excitement because they finally understood where the heck we were going and they were really excited about the strategy.”

- Steve Jobs

I’m sure there’s some Jobsian reality distortion field in that take, but I think there’s a lot of truth behind the notion employees know.

Employees can differentiate between what’s truly “long term” and what’s lip service. They know when “the emperor has no clothes”.

When CEO Brian Chesky shared his vision for Airbnb and the “infinite” time horizon in 2018, the response from some employees were telling:

Internal message boards filled with lamentation and expressions of concern for the future of the company, its financial discipline and their stock. Some workers wrote messages mocking Chesky, who had recently given a presentation about building a 21st-century company with an “infinite time horizon.” Employees joked that they couldn’t wait that long.

Founders pursuing and evangelizing the “long term” is an evergreen concept, but the challenge always lies in the implementation. Pursuing a “long term” vision is not simply a top down mandate. It requires buy-in from all stakeholders, especially the employees. It also requires authenticity or cynicism and loss of confidence takes root.

So when employees are pushing management to go public, that’s a “tell” to me. Yes, some employees are concerned about their equity expiring worthless, but they’re also perceptive that the founders and early employees have little financial incentive to go public having already cashed in hundreds of millions of dollars worth of equity.

In many ways, the groundswell of employees asking to go public is their way of saying “the emperor has no clothes”.

Man in the Mirror

Back in 2010, CEO Brian Chesky gave one of my favorite Startup School talks (part 1, part 2) discussing Airbnb’s early days.

One story that really stuck out to me was the founders pasting a revenue graph on their bathroom mirror as motivation to achieve “ramen profitability” before Y-Combinator Demo Day. It was the first and last thing they looked at everyday.

While the COVID-19 pandemic was an unfortunate setback for Airbnb, it may turn out being a blessing in disguise. There is a tremendous opportunity to rebuild trust with all stakeholders and prove without a doubt CEO Brian Chesky is a true “long term” steward of the company.

Just like the early days, the company will be forced to focus and prioritize.

It would only be appropriate to end his time as a private company the same way he started it, with a graph pasted on the bathroom mirror.