What's it 2U...When Equity is Granted?!

What's it 2U...When Equity is Granted?!

Examining Insider Activity at 2U, Inc.

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

There’s a game of “compensation poker” happening right now where you get to decide if the Company’s most recent equity grant to management is a material “tell”.

2U, Inc. (ticker: TWOU) recently disclosed they granted equity to their CEO and management team ahead of 2019 Fourth Quarter Earnings (February 6, 2020) which has piqued my curiosity.

The timing feels off to me and thought it would be interesting to dig in a bit and speculate on what it may mean for TWOU shareholders.

What’s it to you…when equity is granted?!

Disclaimer: This post is speculative and not definitive. It’s for entertainment purposes only and not investment advice.

Good chance the Company says: “What’s it to you…when equity is granted?!” (i.e. Mind your business. There’s nothing here.)

Announcing Premium Newsletter

Before we dig in, a quick announcement!

First, thank you for reading this newsletter. I appreciate your support and all the positive feedback I’ve received.

Beginning this month (February 2020), I will also be writing premium content for this newsletter that focuses on:

Researching technology stocks (i.e. deep dives, initiations, strategy, unit economics, etc.)

Doing valuation work

Direct listings and IPO breakdowns

Interviewing experts/investors (rolodex permitting) and management

Critiquing activist situations I find interesting

“Real time” situations I think warrant extra attention

(Possibly) Identifying and speculating on equity grants that exhibit “spring loading” and/or “bullet dodging” (No guarantees I’ll find anything worth discussing so can’t fully commit to it)

Companies and industries I think are undergoing an interesting inflection

This post on TWOU is a test run of premium content. Going forward, content like this would fall under the premium umbrella (i.e. Identify and speculate on potential equity grants that exhibit “spring loading”).

Overall, the goal for premium is to create content that’s helpful (and ideally differentiated) to professional and experienced investors. Basically, I’m treating the premium newsletter like a pseudo buyside gig where I’m emailing subscribers as I make progress on various research projects. I will NOT be giving investment advice.

Anyway, thank for supporting my newsletter and back to TWOU!

Read the Man, Not the Cards

In my Profiting from Corporate Governance “Dark Arts” series, I talk about changes in compensation and grant timing as potential “tells” and the importance of understanding the “why” behind those changes. Usually the changes means nothing, but occasionally it hints to something very material:

If you can correctly read the motives of the comp committee (chair) and recognize a material “spring load” or “bullet dodge” is happening, you can trade alongside management’s greed and profit.

TWOU is currently playing a game of “compensation poker” where you get to decide if the Company’s most recent equity grant to management is a material “tell”.

This post is an attempt to “read the man, not the cards” meaning I’m going to focus on the actions of the Board (“the man”) and not dig into the fundamentals (“the cards”).

Please do your own homework before you decide to “fold, call, or raise” on the stock. (Seriously, this post isn’t investment advice)

For those unfamiliar with TWOU, they are an “Educational Technology Company” that contracts with nonprofit colleges and universities to offer online degree programs. The Company supplies its client institutions with a cloud-based software-as-a-service platform, coursework design, infrastructural support, and capital to deliver instruction.

Again, this is not investment advice and be aware TWOU has historically been a battleground stock between longs and shorts.

Sell-Offs Create Focus

I like to follow companies that experience material sell-offs to “war game” what the Board and management is potentially thinking, and speculate on how they may approach and maneuver a “turnaround”.

Much of my previous professional investing experience is tied to understanding (and correctly prescribing) the post sell-off dynamic at companies, and I still enjoy thinking about and discussing these issues.

It’s a major contributing factor to starting this newsletter!

So what do I mean by “war gaming” post sell-off situations?

If you follow me on Twitter, you’ve probably already seen my tweet storm on Grubhub and my “war gaming” speculation that Grubhub pushed themselves and the rest of the food delivery industry into strategic alternatives mode after obliterating the stock -43% with their infamous letter:

Feel free to click through and read the whole tweet storm. Overall, the Grubhub story is still ongoing, but it’s more or less playing out as I expected, and captures the kind of “war gaming” I like to do.

For a more thorough “war gaming” analysis, you can check out my post on e.l.f. Cosmetics and the activist game theory exercise I did.

People sometimes forget that companies are, at the end of the day, run by people with their own aspirations, concerns, stresses, hopes, dreams, etc.

Understand what the people on the ship are thinking and you’ll have a better idea of where they (potentially) steer the ship. Don’t underestimate social dynamics and human behavior, and how those factors can drive and/or destroy shareholder value.

In particular, pay attention to “stressful” situations and how that may influence decision-making.

In my post on Investing with Mindfulness, I discuss the impact of volatility and material sell-offs on executives:

Personal observation but market volatility has a tendency of nudging CEOs who are already sitting on the strategic alternatives fence towards selling. Might not happen right away, but volatility tends to be the catalyst to begin the selling process. It happened in tech after the February 2016 sell-off and a similar dynamic occurred during the Q4 2018 market sell-off.

For example, we saw how the market sell-off in Q4 2018 potentially “nudged” the leadership at Instructure to begin entertaining strategic alternative discussions in January 2019 and ultimately announcing a deal with Thoma Bravo in December 2019. TWOU (in my opinion) seems to be heading in a similar direction as Instructure.

TWOU is a situation I’ve been casually following since the stock experienced a massive sell-off last year, dropping -65% on July 31, 2019 following revised forward guidance.

Dramatic downward stock moves like this pretty much guarantee “casualties” (i.e. headcount restructuring, executive turnover, etc.) of some sort as the Company attempts to re-focus and re-prioritize. In the case of TWOU, the Company announced on August 22, 2019 (3 weeks after revising guidance) that the CFO would be “retiring”. There’s still a ton of pressure to turnaround the Company so I would not rule out additional “casualties” down the road.

Insider Trading Activity

When meaningful sell-offs occur, I also pay attention to insider trading and equity grant activity.

As previously discussed in my post about Entertainment One’s acquisition by Hasbro, insider transactions by management and Board members following a sell-off can be a useful signal. Insider buying from executives can be “hit or miss” (they could be “bluffing” to encourage confidence in the market), but the signal gets interesting when Board members begin buying the stock (as was the case at Entertainment One).

So what did insider activity look like at TWOU following the stock’s July 2019 blow up? Several Board members were buying stock:

A few high level takeaways:

It’s not often you see 4 Directors (and 1 COO) making open market purchases.

Aside from Edward Macias (who has an academic career background and still acquired $50,000 worth of stock), the other insiders bought a meaningful amount of stock ranging from $500K to $1M. You especially don’t see Directors buying in size like that.

Gregory Peters “doubled down” (and averaged down) buying $1M worth of stock having previously acquired $1M worth of stock in 2 separate transactions ($500K per transaction). This also highlights the risk of blindly trading alongside insiders. If you had traded alongside Gregory Peters’ previous 2 trades, you’d be underwater in your position.

Robert Stavis is from Bessemer and should have a good feel for valuation and opportunity.

John Larson is Chair of the Compensation Committee. If he thinks the stock is “cheap”, that should inform your thinking when evaluating the compensation committee equity granting decisions.

Overall, the market considered this buying activity pretty bullish and the stock responded accordingly appreciating ~40% by the end of August 2019 from the July 2019 low and ~25%+ from when Directors were purchasing stock. That said, the stock has remained largely range bound in the high teens and low $20s since September 2019.

Activist Investors on the Horizon

In addition to the internal stress of operating a turnaround, sell-offs also ramp up external stress as public shareholders privately (and sometimes publicly) express their dissatisfaction with the Company and demand answers. This in turn creates even more internal pressure for the Board and management team to fix the issues and have answers. Call it a “stress flywheel” if you will.

And whenever a Company’s strategic direction is up for serious debate (as is usually the case post sell-off), you can expect activists to show up. Companies are especially vulnerable to activist investors when price weakness occurs close to “activist season” (generally begins in November).

I describe “activist season” in my post on e.l.f. Cosmetics (ELF) when I discussed ELF’s vulnerability to a contested 2020 election:

“Activist season” is a phrase I use to describe the time of year (typically around the holidays…fun!) when activists and targeted Companies are quietly maneuvering (possibly negotiating with each other) in anticipation of the Director nomination period when activists can submit nominees for a potential proxy contest.

In the case of TWOU, an activist did show up and is pushing the Company to pursue strategic alternatives (as reported in November…activist season operates like clockwork). It was also recently reported that the Company is now weighing a potential sale:

2U Inc. has hired advisers for a strategic review after an activist investor pressured the educational software company to explore a sale, according to people familiar with the matter.

We’ll see how things play out but the Company’s recent equity grant to management seems to indicate a transaction is firmly on the table.

“Spring Load” Equity Grant?

Let me reiterate it again:

You should always pay attention to changes in compensation.

As previously discussed in the the “Dark Arts” series:

Changes in compensation and grant timing are “tells” (to borrow a poker term) so it’s important to understand the “why” behind those changes. Usually the changes means nothing, but occasionally it hints to something very material.

If you can correctly read the motives of the comp committee (chair) and recognize a material “spring load” or “bullet dodge” is happening, you can trade alongside management’s greed and profit.

As a reminder, “spring loading” is when a Company grants equity to management and then releases news that positively impacts the stock price.

Given the pressure to turnaround the Company and/or seek strategic alternatives, did TWOU just “spring load” equity grants to management in anticipation of “positive” news?

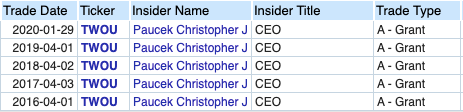

Let’s take a look at the equity grant history of CEO Christopher "Chip" Paucek for his last 5 grants.

Notice something different?

Historically (recent history), TWOU granted equity in early April AFTER fourth quarter earnings and forward annual guidance was already given (in late February).

This year, they granted equity in January a week BEFORE 2019 fourth quarter earnings and (presumably) 2020 annual guidance.

I find this interesting for a few reasons:

Annual equity grant best practice is to grant equity a few days after fourth quarter earnings release. The Compensation Committee decided to grant before earnings.

When changes to compensation occur, there’s usually a lot of thought and care into making those changes. The Compensation Committee explicitly decided to grant equity before the earnings release date. It’s not an oversight the Compensation Committee decided to grant equity before earnings instead of after earnings.

There is clearly a lot of pressure to have a plan in place to maximize shareholder value in 2020 following the July 2019 sell-off. Fourth quarter 2019 earnings is an incredibly important check-in with shareholders to communicate TWOU’s go-forward plan, and the stock could materially move on what is said.

The grant occurred a week before earnings. Management and the Board knows what they are going to say and the valuation impact that is going to have. If the news was “bad”, management would be (in my opinion) advocating for “best practices” and receive equity post earnings (after the stock price materially resets on the “bad” news). Instead, they got equity before earnings.

Given theres’s already strategic alternative chatter, granting equity before addressing that chatter is peculiar.

The Company also moved up their earnings release date to February 6, 2020 from their typical late February reporting pattern.

We can only speculate to why the Company moved up earnings, but the Director nomination window begins in late February and the Company may want to put out incrementally positive guidance and officially address strategic alternatives as soon as possible to preempt shareholder pressure (and an activist Director slate).

Also, if you take a look at the CEO’s 2020 equity grant and compare it to his 2019 equity grant, the equity composition changed from a combination of restricted stock units (RSUs) and stock options in 2019 to RSUs only (that we’re aware of) in 2020.

I say “that we’re aware of” because the Company isn’t obligated to disclose equity with performance-based hurdles tied to them (normally called “Performance Stock Units” or PSUs) in Form 4 filings and I suspect PSUs are in the mix here.

This is a completely anecdotal take, but companies have a propensity of changing equity composition when their mindset shifts towards strategic alternatives or there’s a meaningful change to strategy.

So “why” would these changes happen? Is it a “spring load” grant?

That’s up to you to decide!

Given the activist chatter, strategic alternatives talk, and key dates (earnings/guidance and nomination window), you can piece together a pretty compelling case that this is potentially a “spring load” equity grant, but nothing is guaranteed when it comes to investing and markets.

Remember, we’re just “reading the man” and this writeup isn’t contemplating the fundamentals and is speculation.

What’s Next?

Your guess is as good as mine.

It will be interesting to see what management has to say on their February 6, 2020 earnings call and the annual guidance they give out.

Will they officially announce strategic alternatives? Did they purposely move the earnings date up with the hope of sharing good news?

While there are signs that a “spring load” grant is at play, you can’t totally dismiss a scenario where management kitchen sinks (or suspends) annual guidance or communicates incrementally bad news.

Also, even if a transaction is on the table, there’s no guarantee a deal will occur or that a deal will occur at a premium shareholders will approve.

Overall, this is why corporate governance so interesting to me. It’s about the people.

Understand what the people on the ship are thinking and you’ll have a better idea of where they (potentially) steer the ship. Know where the ship is going and you’ll find interesting risk-adjusted investment opportunities.