The (Vax)Art of Well-Timed Insider Transactions

The (Vax)Art of Well-Timed Insider Transactions

Corporate Governance is in the Eye of the Beholder

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

Premium Subscriber Note: There’s a premium companion piece to this write-up. It examines how incentive structures can (ex ante) signal material nonpublic information (MNPI) using Vaxart as a case study. On to the write-up…

Corporate Governance is in the Eye of the Beholder

Critiquing corporate governance often entails piecing together what happened to make inferences on why it happened. Once you understand the what and the why, you’ll be surprised how many risk-adjusted investment opportunities present themselves.

The challenge is (as outsiders) we never get the full picture on the what and the why so we’re forced to make inferences using incomplete information. Consequently, my interpretation of a situation may be completely different from someone else’s interpretation. It’s all in the eye of the beholder, and that’s fine.

For instance, consider this scenario:

You’re a Board member in possession of material, nonpublic information (MNPI) that will potentially 3x to 5x the company’s stock when it’s released.

You also own ~30% of the company (via stock and warrants) which arguably makes you one of the most powerful and influential directors on the Board.

Insider trading on MNPI is obviously prohibited, but you’re open to rewarding insiders for a job well done. After all the stock is going to 3x to 5x!

Given your large ownership stake, you also want to lock in anticipated/expected gains. There’s going to be a lot of volume/demand following the release of MNPI and there’s no certainty prices will remain elevated.

What levers can you pull to maximize value for yourself and insiders? Which levers do you think are appropriate vs. inappropriate?

The answer isn’t always straightforward.

Luckily for us, this scenario isn’t hypothetical and we can examine real decisions made by insiders at vaccine biotech Vaxart (ticker: VXRT) leading up to and following their announced selection to the U.S. government’s COVID-19 vaccine program Operation Warp Speed.

The “Dark Art” of Profiting on MNPI and Avoiding Scrutiny

I’ve seen my fair share of (aggressive) insider transactions over the years, but Vaxart may have pulled off one of the greatest spring load equity grants of all time by granting options (at strike prices below $2.50) before publicly announcing MNPI that would push the stock up as high as $14.30 per share ~2 to 3 weeks later.

How is this possible?

While insider trading is prohibited when in possession of MNPI, the world of equity compensation is a bit different. There’s a lot more grey area and a lot less scrutiny/outrage when it comes to granting equity while in possession of MNPI.

And yes, if you were paying attention, you could have inferred (mosaic theory ftw!) something big was on the table at Vaxart and traded alongside. (Full disclosure: I don’t cover this in the write-up.)

How Vaxart was able to avoid scrutiny and criticism for their equity transactions while fellow biotech Moderna continues to face intense scrutiny and criticism for their equity transactions is top notch corporate governance “dark arts”.

“I’m a Biotech Tourist” Disclaimer

Before we dive in further, a quick disclaimer/warning. I’m a biotech tourist and don’t follow the space closely. Vaxart fell into my lap due to an inbound governance/compensation question on the company.

Consequently, this write-up is primarily a “play the man, not the cards” type analysis. Apologies in advance if my assessment is off base. This my interpretation of the situation and I could be wrong or have missed key facts that would change my opinion since I don’t cover Biotech.

Vaxart: “Vaccine as a Pill”

Vaxart provides a pretty good layman presentation on the company and their COVID-19 vaccine opportunity, but high-level the company presents themselves as a “disruptive oral vaccine platform”:

Vaxart’s “vaccine as a pill” approach is a convenient mode of administration with no needles and is self administered (no appointments, no lines, social distancing).

The company believes they potentially have best-in-class efficacy against COVID-19 and other airborne viruses.

The pill form factor allows for low cost distribution and storage. It requires no refrigeration and is room-temperature stable.

The company is currently working on several vaccines candidates including an oral vaccine for COVID-19.

Assuming Vaxart’s science/technology is legitimate (I’m told it’s legitimate for what it’s worth) and their COVID-19 oral vaccine is approved, the belief is the stock will be a big winner.

This makes intuitive sense to me as a casual observer. If given the choice and all else being equal, I would definitely prefer ingesting a vaccine pill over getting a vaccine shot.

Vaxart’s Memorable 2020 (Year-to-Date)

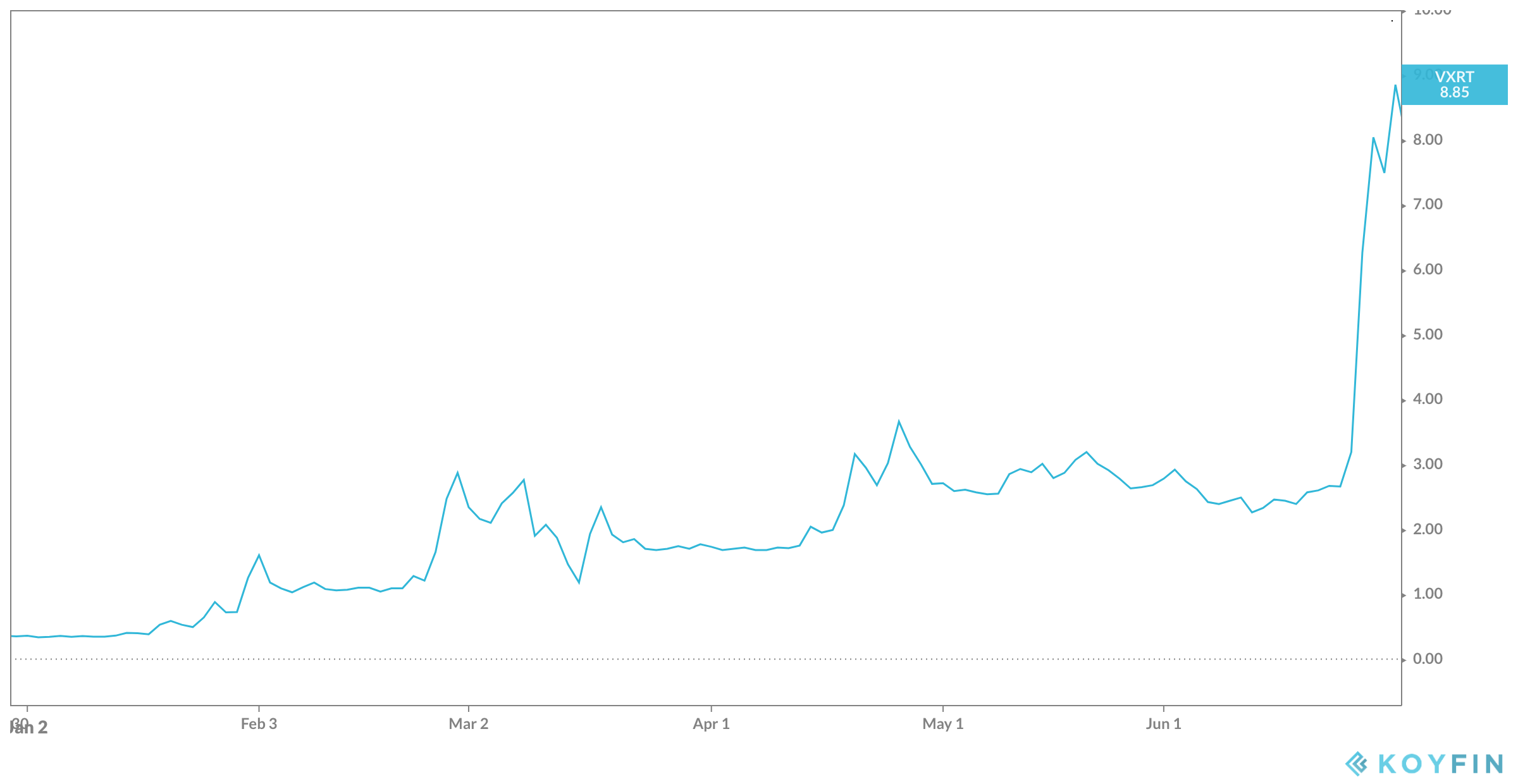

It’s an understatement to say 2020 has been a memorable year for Vaxart. The stock started 2020 at $0.35 per share and closed June 30, 2020 at $8.85.

Motley Fool has a nice summary on Vaxart’s year-to-date performance, but it’s fair to say much of the stock’s phenomenal run in 2020 is tied to positive news flow around the company’s development of a COVID-19 oral vaccine.

In fact, the most significant stock pop of 2020 can be attributed to Vaxart’s June 26, 2020 announcement that the company’s COVID-19 oral vaccine is 1 of 7 vaccine candidates selected to participate in the U.S. government’s Operation Warp Speed program to develop a COVID-19 vaccine by January 2021.

Did Vaxart “Spring Load” Equity Before Releasing MNPI?

While Vaxart announced their inclusion in Operation Warp Speed on June 26, 2020, the big question is when did Vaxart actually know they were selected to Operation Warp Speed?

I suspect they knew of their selection in Operation Warp Speed as early as June 3, 2020, and potentially sat on this MNPI to the benefit of insiders who were subsequently granted options at low strike prices.

I say as early as June 3, 2020, because Bloomberg reported on June 3rd that The White House was working with seven companies (5 known, 2 unknown) as part of its “Warp Speed” COVID-19 vaccine program:

The companies include Johnson & Johnson, Merck & Co., Pfizer Inc., the Cambridge, Massachusetts-based biotech Moderna Inc., and the University of Oxford in collaboration with AstraZeneca Plc, as well as two other firms, according to two people familiar with the matter.

Coincidentally, ~30% shareholder Armistice Capital (who has 2 board seats) also appears to pause their aggressive selling of Vaxart stock on June 3, 2020 and doesn’t restart selling until June 26, 2020 after Vaxart announces their selection to Operation Warp Speed.

This “pause” in selling by Armistice Capital aligns with Bloomberg’s June 3rd reporting and potentially signals Vaxart implemented an insider trading blackout period upon notification by The White House they were selected for Operation Warp Speed.

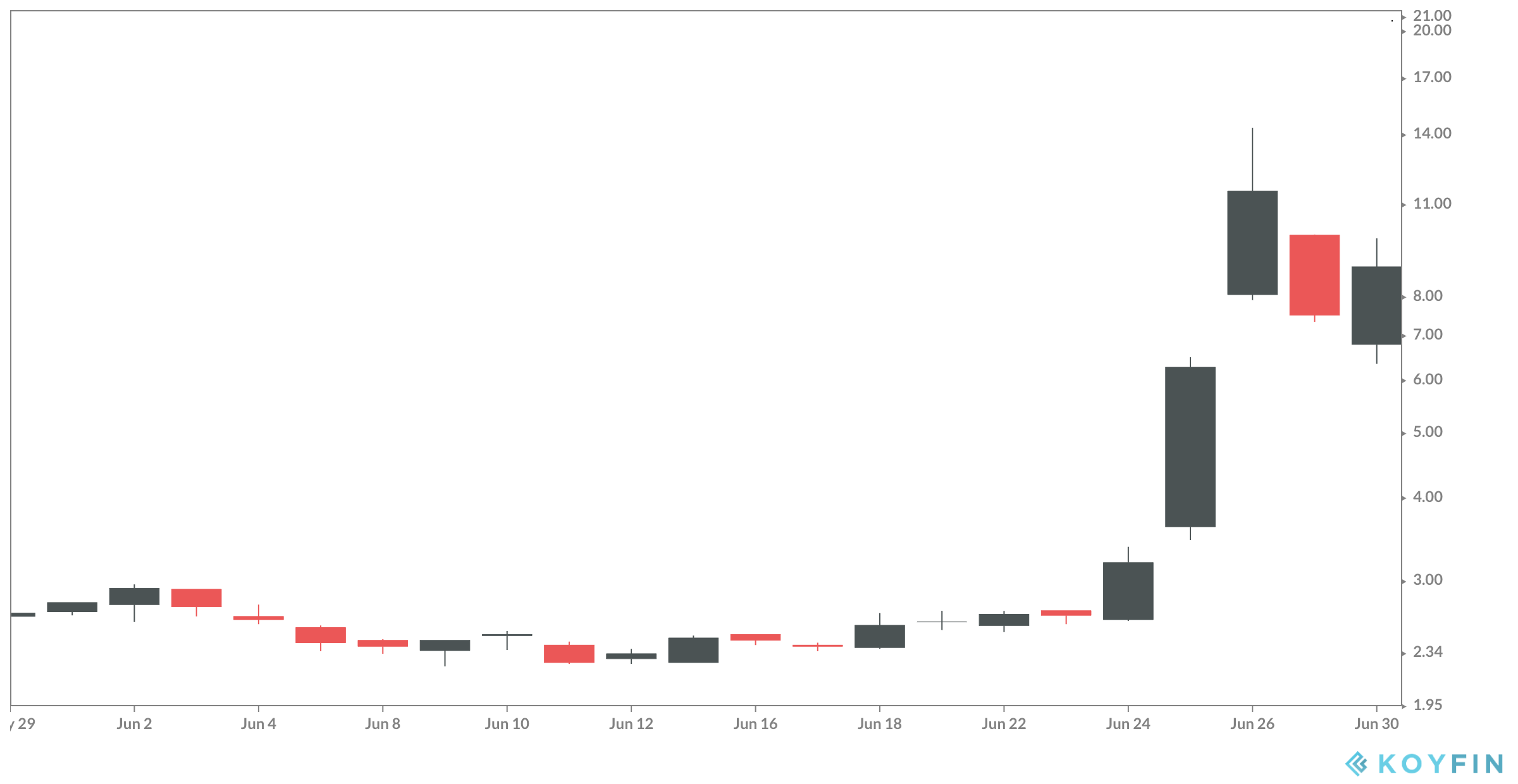

If Vaxart was indeed 1 of the 2 unnamed companies in Bloomberg’s June 3rd report, Vaxart’s June 2020 equity grants is one of the greatest “spring load” equity transactions ever. As a reminder, “spring loading” is when a company grants equity while in possession of MNPI and then releases news that positively impacts the stock price:

This hypothetical “spring load” chart looks exaggerated, but take a look at Vaxart’s June 2020 price chart and realize equity was granted to insiders on June 8 and June 15 (to a new CEO with some interesting terms) below $2.50 per share and before the (coordinated?) sequential release of MNPI on June 24 (Russell 3000 Index inclusion), June 25 (COVID-19 vaccine manufacturing deal), and June 26 (Operation Warp Speed announcement) which would push the stock up as high as $14.30 per share before re-settling in the $7s to $8s:

Simply put, June 2020 was an incredible month for Vaxart and insiders.

The Influence of Armistice Capital

Whenever I see clever corporate governance maneuvers, I naturally ask myself “who is pulling the strings here?”. You never know for sure who’s pulling the strings, but in the case of Vaxart all roads seem to converge to Armistice Capital who owned ~30% and had 2 Board seats.

First of all, you know you’re a major power broker when you get your own 10-K risk factor disclosure:

Armistice owns a significant percentage of our outstanding shares of common stock and will be able to exert significant control over matters subject to shareholder approval.

Armistice has the ability to substantially influence us and exert significant control through this ownership position. Armistice may significantly influence the elections of directors, issuance of equity, including to our employees under equity incentive plans, amendments of our organizational documents, or approval of any merger, sale of assets or other major corporate transaction. Armistice’s interests may not always align with our corporate interests or the interests of other stockholders, and it may exercise its voting and other rights in a manner with which our other stockholders may not agree or that may not be in the best interests of our other stockholders.

I could probably do an entire write-up on what I think are Armistice influenced decisions at Vaxart, but for the sake of keeping this write-up manageable I’m not going to do that.

That said, there’s one low key decision I wanted to highlight that I believe was influenced by Armistice and I find really interesting (as a governance nerd).

Weeks before releasing MNPI, Vaxart amended (on June 8, 2020) their warrant agreement with Armistice Capital that would make it easier for Armistice to aggressively exercise their sizable holding of warrants and sell stock.

The ex ante signaling of the amendment is subtle here, but I believe the company wouldn’t agree to this amendment unless they had confidence there would be strong demand for the stock within 60 days of the amendment. Otherwise, Armistice could wreck the stock. I don’t think Armistice would purposely wreck the stock, but they’d have the power to do so after the amendment. Further, I don’t think Armistice would push for an amendment unless they believed/anticipated strong demand for the stock.

The result of this amendment?

Following Vaxart’s June 26, 2020 Operation Warp Speed announcement, Armistice would capitalize on elevated volume/demand by exercising 20.8 million warrants and aggressively selling 27.6 million shares between June 26 and June 29, rapidly reducing their ownership stake from 29% to 0.2%. Without the warrant amendment, I don’t think it be possible for Armistice to exit their Vaxart within one Form 4 disclosure cycle.

Obviously with hindsight we can infer that the amendment is likely linked to Vaxart’s selection to Operation Warp Speed, but you could have deduced in “real time” something big was potentially on the table. Pretty cool, huh?

What an incredible exit for Armistice Capital.

The Art (and Turpentine) of Corporate Governance

Let me reiterate again, this is my interpretation of the insider transactions at Vaxart and I could be off base. Studying corporate governance can feel a lot like studying art at times (stop laughing). We can all look at the same piece of art, and have completely different opinions and takeaways. As Pablo Picasso once said:

“When art critics get together they talk about form and structure and meaning. When artists get together they talk about where you can buy cheap turpentine.”

Some are focused on the form and structure of governance. Some are focused on where to find a competent director (preferably with an investor perspective). I probably sit somewhere in the middle.