Corp Governance "Dark Arts": Part 5

Corp Governance "Dark Arts": Part 5

Kodak Case Study: Aggressive 2020 Insider Transactions

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

Welcome to Part 5 of the ongoing Corporate Governance “Dark Arts” series!

For Part 5, I’m covering Kodak (ticker: KODK) and the Board’s aggressive 2020 equity grant practices to management and to themselves! We usually just focus on executive compensation so it’s nice to shine a light on director compensation “dark arts” as well.

In particular, Kodak double dipped director equity grants (January 2020 RSUs and May 2020 options), and granted executives options a day before announcing a $765 million government loan that would pop the stock from ~$2.50 to ~$33.

Kodak is an excellent example of insiders manipulating the timing and type of equity grants while in possession of material nonpublic information to harvest excess value.

Note: Kodak’s Board discussing the “dark art” of leveraging best practices to maximize equity grants to themselves.

Corporate Governance “Dark Arts” Series

Note: Feel free to skip this section if you’re familiar with the series.

For those unfamiliar with the “Dark Art” series, it’s an ongoing series where I discuss (through explainers and case studies) how companies use the “Dark Arts” of corporate governance to:

Take Advantage of Unsuspecting Shareholders and Directors

Influence Decision-Making

Profit

And yes, if you know what you’re doing, there are windows of opportunity to participate alongside.

If you’re new to the “Dark Arts”, I highly recommend reading Part 1 which provides a pretty thorough run down of the basics and high-level concepts. I also provide an abbreviated summary of key concepts below so you’re not completely lost with what’s going on.

For Part 2, I walk you through a case study that features TPG, their co-CEO Jim Coulter, and the infamous acquisition of J. Crew.

For Part 3, I cover Stamps.com (ticker: STMP) and walk you through the company’s legendary (to me) 2019 options grant to management.

For Part 4, I show you how I develop a “big picture” view of proxy disclosures and critique GreenSky’s (ticker: GSKY) aggressive equity grant practices.

Finally, for the podcast listeners out there, I also discuss the “dark arts” on Tobias Carlisle’s Acquirer’s Multiple Podcast:

Key Concepts from “Dark Arts” Part 1

Note: Feel free to skip this section if you’re familiar with the key concepts.

Part 1 of Corporate Governance “Dark Arts” series focuses on the basics and high-level concepts of “dark” governance actions on the Board (especially actions tied to compensation).

I define the “Dark Arts” as actions that distort Management-Board-Shareholder alignment to primarily benefit insiders (who engage in the “dark” action) and to gain disproportionate control and/or influence over the governance process.

This does not necessarily mean the “Dark Arts” are illegal.

Compensation is the most important area to understand when examining corporate governance “Dark Arts”.

Compensation best practices noticeably die first when exposed to “dark” actions. That’s your signal to examine the situation closer.

The compensation committee chair is arguably the most powerful “independent” position on the Board, and can singlehandedly distort the power dynamics of the entire Board.

Of all the “dark” actions, monitoring equity grants is the most important. In particular, pay extra attention to “spring loading” and “bullet dodging” behavior.

Manipulating the timing of equity grants relative to material news releases is an easy way for insiders to capture value in excess of “target value”. If you can recognize the signs of this practice, you can profitably participate alongside. No, the SEC does not appear interested in cracking down on this behavior.

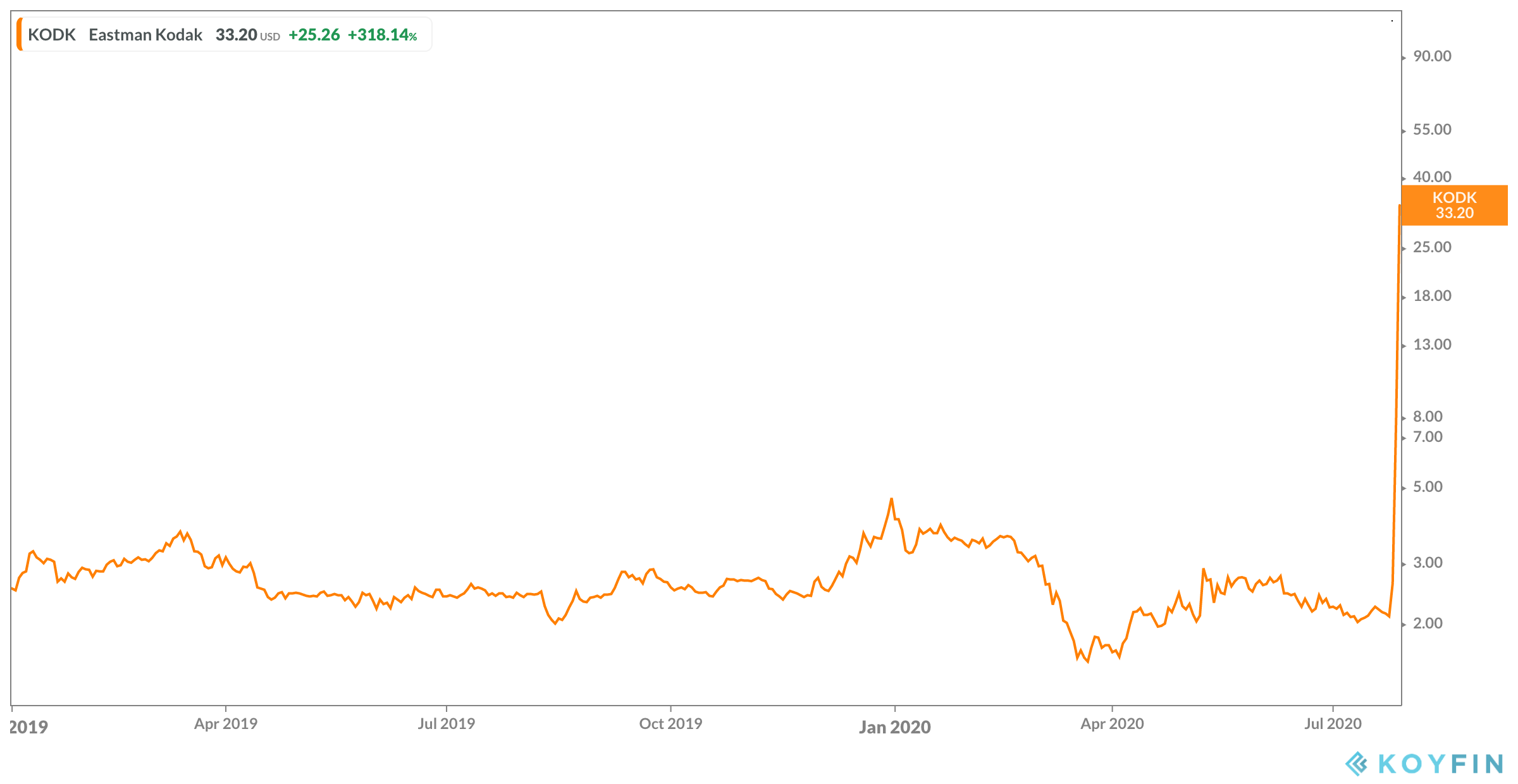

Kodak’s Momentous Announcement

On July 29, 2020, Kodak’s stock moved an eye popping 300% after announcing a deal with the U.S. government to pivot into drug production with the help of a $765 million government loan:

Eastman Kodak Co. has won a $765 million government loan under the Defense Production Act, the first of its kind. The purpose: to help expedite domestic production of drugs that can treat a variety of medical conditions and loosen the U.S. reliance on foreign sources.

The onetime leader in photography sales is gearing up to produce ingredients for a number of generic drugs, including the antimalarial drug hydroxychloroquine that President Trump has touted in the treatment of coronavirus. Meanwhile, the U.S. is aiming to shift from relying on countries such as China and India, Kodak Chief Executive Jim Continenza and U.S. officials said. (WSJ)

According to Executive Chairman James Continenza, the deal came together over the last couple months:

“The DFC, I call them a translator, we’re a business, they’re government, we don’t speak the same language and they were the translator and they made it really simple for us to understand and navigate through it and Dr. Navarro does not take enough credit for what he did. He’s the one who was like, ‘can you do this, get to the point, get it done, bye.’ This was literally two months ago that’s how fast this has been moving, but it was every day. Once you’re in, you’re in. I was joking, we were given five days by Dr. Navarro, he calls it Trump Time, and I learned what that is to get this done and we did it in four because I said Trump Time is five, we’re going to do better, we have to do better and my team did and it was amazing.” (interview)

When I come across exaggerated price moves like what occurred at Kodak, I always look for potential ex-ante signals. It’s partly out of curiosity and partly for future reference.

You’d be surprised how often insiders “tip” they possess material nonpublic information. Their behavior exhibits signs of “trembling with greed” and they push the envelope on governance to get their “fair share” of the upside.

Ask yourself, if you possessed material nonpublic information, what (legal-ish) levers could you pull to maximize your financial upside?

There are several things you can do, but in the case of Kodak (assuming they were aware of a potential deal in May 2020):

They kept the insider trading window open.

Moved the timing and type of director equity grants.

Granted executives spring loaded options a day before announcing the deal.

Overall, if you were paying attention, I’d argue Kodak was signaling something potentially material was on the table 2 months ago. This also aligns with Kodak’s commentary that talks with the U.S. government started 2 months ago.

History of Insider Buying

There’s plenty of coverage and scrutiny regarding recent insider buying activity at Kodak so I’m not going to spend too much time on it.

I will say, of all the things to give insiders a hard time for, criticism over their insider buying activity detracts from the more egregious decisions around equity grants which deserve genuine scrutiny and investigation.

I get it though, exploring the possibility of nefarious insider trading is “low hanging fruit” journalism and grabs people’s attention.

That said, it’s hard for me to create a strong “gotcha” insider trading narrative here. It’s no secret insiders want to own more Kodak stock, and have been proactively buying stock in the open market the last couple years:

Source: Openinsider.com

If you really wanted to criticize the insider buying, I’d spend less time on the buying and more time on why the open market trading window remained opened.

When in possession of material nonpublic information, companies should proactively close their regularly scheduled trading windows. The issue is companies have a lot of leeway determining what’s “material” and (unsurprisingly) insiders don’t want to close the window if they have legal cover to keep it open.

This is how you end up with situations where companies are having earnest M&A conversations to sell themselves (or in the case of Kodak, government loan conversations), but the trading window remains open because there isn’t a formal offer or agreement in place.

While Kodak can argue they didn’t possess material nonpublic information that warranted closing the open market window, their actions related to director compensation says otherwise.

Directors Double Dip on Equity Grants

Most people don’t pay attention to director compensation, because it’s fairly standardized and is less likely to be manipulated when compared to executive compensation.

Typically, directors get an annual equity grant with a few companies (such as Kodak) also giving quarterly equity grants in lieu of cash compensation.

Kodak typically grants annual equity to directors in January in the form of RSUs:

Pursuant to the previous determination of the Board of Directors that annual director grants be made on the fifth trading day of each calendar year commencing with 2016. (Source: 2020 Proxy)

In my experience, this is an atypical grant cadence. You don’t see many companies giving their directors equity in January. In general, annual director equity grants are usually made on the date of the company’s annual meeting or shortly thereafter.

For Kodak, this means if they want to follow director compensation “best practices” they should grant equity in May and not January.

I bring this up, because using “best practices” to justify self-serving decisions is top notch “dark arts”.

No one is going to raise a flag on Kodak directors receiving options on May 20, 2020 the same day as the 2020 annual meeting. The company can also hide behind “best practices” and say they’re re-aligning grants to industry standard practices if someone inquires about the second equity grant.

That said, if you were aware Kodak historically granted RSUs to directors in January, alarm bells should be going off:

Why are directors getting another large grant 4 months later?

Why did the company suddenly switch to options when they historically granted RSUs?

The most intriguing part of the May 2020 option grants is they apply premium exercise prices (vs. grant date stock price of $2.57) that mirror Executive Chairman James Continenza’s February 2019 options grant:

Upon his appointment to the position of Executive Chairman, Mr. Continenza received a grant of stock options under our 2013 Omnibus Incentive Plan (the “Plan”) in 2019. The grant was issued in 4 tranches as follows:

Tranche 1 (1,150,000 stock options) has an exercise price of $3.03, which was the closing price of a share on the grant date;

Tranche 2 (350,000 stock options) has an exercise price of $4.53;

Tranche 3 (350,000 stock options) has an exercise price of $6.03; and

Tranche 4 (200,000 stock options) has an exercise price of $12.

source: 2020 Proxy

This is incredibly unusual:

Why adopt such aggressive premium exercise prices?

What gives the Board confidence to not only switch to options from RSUs, but to grant them with materially high exercise prices?

When you see insiders suddenly accept options with premium strike prices, pay attention. That’s not an arbitrary decision and is explicitly contemplated.

I can only speculate on why the changes occurred at Kodak, but based on past experience this is the kind of behavior you’d see from insiders extremely bullish on the prospects of the company.

And given several directors have proactively purchased Kodak stock over the years, I don’t think it’s a stretch to believe the Board was willing to push the governance envelop to double dip on equity grants and maximize their financial upside.

Remember, these option grants likely overlap government loan conversations. Kodak doesn’t provide a precise timeline on loan talks, but the company coincidentally moved $70 million from a China subsidiary to a U.S. subsidiary in mid May:

On May 12, 2020, a Chinese subsidiary of Kodak transferred approximately $70 million to a U.S. subsidiary of Kodak in anticipation of an inter-company transaction. (10-Q filing)

If you were about to embark on a major manufacturing initiative in the U.S., it makes a lot of sense to move cash to the U.S.

Also, Popular Information points out the White House announced on May 14, a week before options were granted to Kodak directors, their intent to invest in domestic manufacturing capabilities:

The administration's loan to Kodak was possible because of a May 14 announcement by Trump. That was when Trump delegated authority to the CEO of the United States International Development Finance Corporation (DFC) under the Defense Production Act. The DFC was authorized to invest in companies to "restore the domestic industrial base capabilities, including supply chains within the United States… needed to respond to the COVID-19 outbreak."

We don’t definitively know what Kodak’s Board knew, but if you believe the May director option grants overlap government loan discussions, it becomes fairly obvious why the Board would be bullish and happily grant themselves premium exercise price options.

From the outside the grants looks like out-of-the money options, but insiders know they’re actually in-the-money options once a deal is announced.

Executive Option Grants One Day Before Announcement

While there’s uncertainty around the circumstances of the May 2020 option grants and what the Board knew, there is no doubt the Board knew they had a deal for a government loan when they granted options to executives on July 27, 2020.

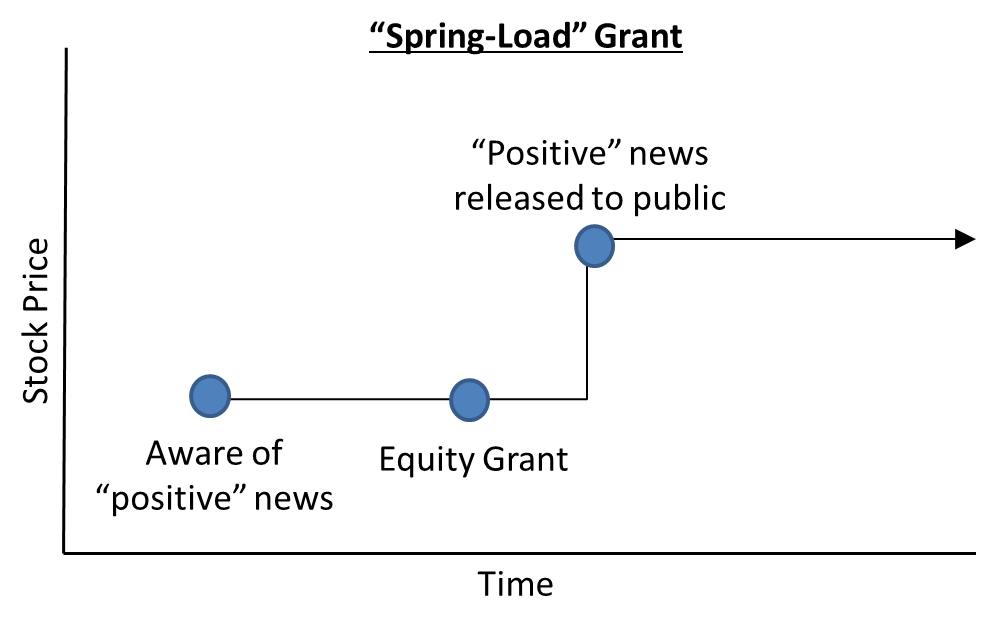

This is a textbook case of “spring loading” equity. As a reminder, “spring loading” is when equity is granted before releasing news that positively impacts the stock price:

Interestingly, the options granted to executives include the same premium exercise prices granted to directors. To me, this somewhat confirms the options (and their premium exercise price structure) were implemented with extreme bullishness in mind.

Anyway, what’s really clever about the grant is it occurred on July 27th.

By granting the options on July 27th, the company doesn’t have to disclose the grants until July 29th. This means they can announce the government loan on July 28th, go on the media PR circuit, and not have the grants scrutinized. By the time the grants are disclosed, the news cycle is over and odds are very low anyone notices the grants and follows up.

It’s funny to think Kodak’s spring load grant was nearly derailed when the deal momentarily leaked on July 27th:

Rochester local CBS news affiliate WROC-TV reported a story with the headline “Kodak, US Government To Unveil A New Manufacturing Initiative In Response To COVID-19 Pandemic” on Monday, July 27 at 11:56 a.m. ET, according to a cached version of the story. The original story has been taken down.

The official press release addressing the news was issued on Tuesday. (source)

The options weren’t granted yet and it be impossible to grant them with the same exercise prices directors received in May 2020 if the leaked news was fully priced into the stock on July 27th.

Ex-Ante Signals via Corporate Governance “Dark Arts”

Overall, you didn’t have to wait for an inadvertent leak to capitalize on Kodak’s stock pop. You could have deducted something material was on the table 2 months ago when directors decided to double dip on equity grants and shifted to options over RSUs.

Corporate governance “dark arts” can surprisingly be good source of ex-ante signals so always pay attention to sudden changes in grant timing, grant type, and price hurdles.

You’ll be surprised how often the same story plays out.

I’ve been reading these Dark Arts case studies which are fascinating, but how do you monitor and screen for these type of actions at the time they occur? It’s not clear to me, without randomly picking companies to keep an eye on, how one can track these activities across the market?